Revealing Insights

AI is rewriting the

entertainment industry.

I'm Andrew Rosen, founder of PARQOR. Through The Medium newsletter, I analyze how artificial intelligence, M&A, and shifting power dynamics are reshaping Hollywood, streaming, and content rights.

What is PARQOR?

How to pronounce: “Paar - kor”

PARQOR reflects the mindset of revealing hidden patterns in marketplaces.

The branding is a nod to parkour, the practice of navigating urban environments creatively and efficiently.

About

A former executive-turned-analyst tracking how AI is reshaping entertainment

I am Andrew Rosen. Puck News recently described me as “the digital media savant.”

I started my executive career in 2005 when Google's Search Engine Optimization and direct-to-consumer became the new paradigms. Inside the building, I learned what the smartest executives were missing or struggling to understand.

I then cut my teeth as a media and technology analyst during the streaming era, including writing the Medium Shift column for The Information.

Now, with over 20 years of experience in digital media, I track how generative AI is a fundamentally new medium—not just history repeating itself.

Our analysis has been cited by The Information, Variety, Deadline and Wired, among others.

Latest from The Medium

Recent analysis

Why "Internet Collaborative IP" Catapulted Two YouTubers Past Star Wars

A significant development for an emerging generation of generative AI creators who have—and have not—built communities....

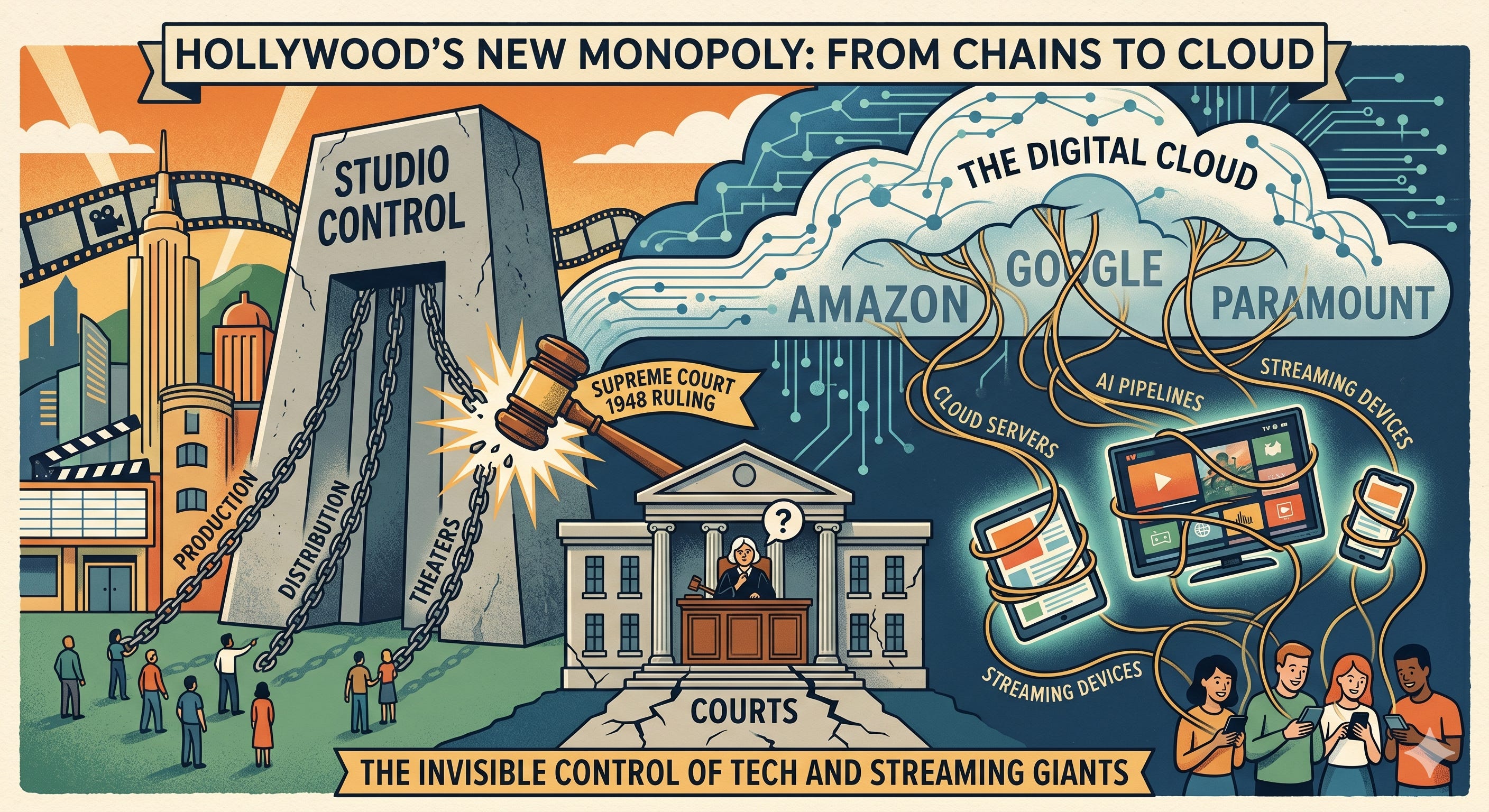

The New Vertical Integration: How Amazon, Google and Paramount + Oracle Are Rewriting the Paramount Decrees

In post- Paramount Decrees Hollywood, vertical integration is emerging with AI and cloud infrastructure instead of theater chains....

Two Amazon AI Original Series Deals Went Wrong in 48 Hours. Here's Why They Matter.

What went wrong for director Jorge Gutierrez and creator Loryn Brantz reveals who wins and loses when tech companies and studios start buying up AI rights....

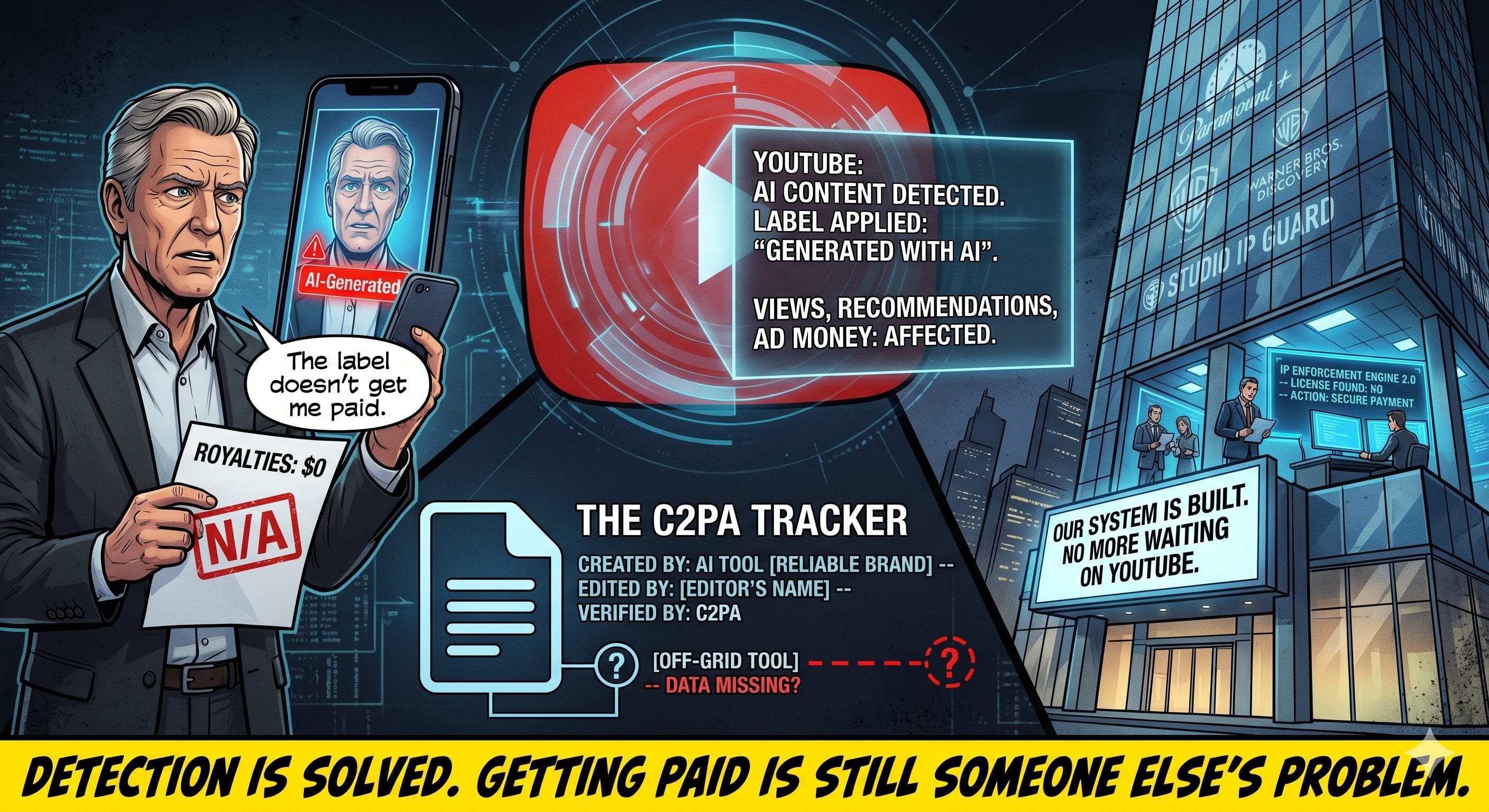

YouTube Figured Out How to Spot AI Videos. Monetizing Them Is Someone Else's Problem.

Inside the gap between detection and compensation—and who's betting they can close it first....

Hollywood Just Drew a Line in the Sand on AI Actors... which Bollywood Already Crossed.

What the new SAG-AFTRA deal actually says—and why the real test is when anyone enforces it....

From PARQOR

Accorde AI Studios

Trust infrastructure for AI in Hollywood. A neutral governance lab helping studios, guilds, and creative workers find AI use cases that are contract-compliant, talent-acceptable, and publicly defensible.

Pilot design. Use-case review. Consent workflows. Governance templates. Risk classification. Certification.

Learn more at Accorde.ai